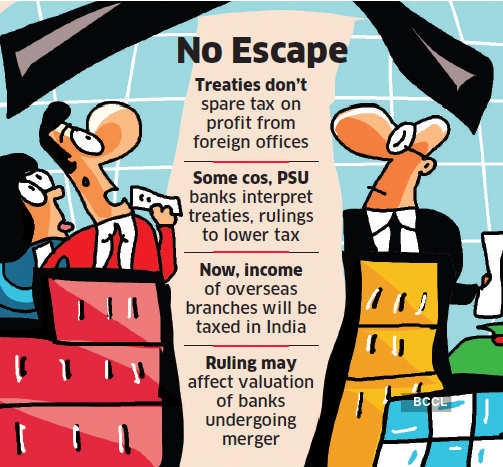

Mumbai: For years, many companies, including some public sector banks, have interpreted India’s treaty provisions with other countries in a way to escape tax on profits from foreign offices. A ruling this month by the Mumbai bench of the Income Tax Appellate Tribunal (ITAT) will put an end to this.

The practice continued even after 2008 when the tax law was amended to clarify that India may tax earnings of overseas branches. Several companies still avoided tax by citing earlier court decisions that seemed to favour their interpretation.

“This will change. The recent decision by the ITAT, Mumbai may impact the valuation of some of the nationalised banks which are undergoing merger. Till now, these banks have been disputing the position in the law and not paying tax on earnings of overseas branches,” said senior chartered accountant Dilip Lakhani.

For instance, an entity with Rs 100 crore profits from Indian operations and Rs 20 crore from its Dubai branches paid tax in India only on Rs 100 crore (and not Rs 120 crore) on the back of the argument that since its foreign branches create ‘permanent establishments’ in UAE and the income from the same is liable to tax in the foreign country, the income from overseas offices should be exempt in India.

“The interpretation, particularly prior to 2008, was like this: Income of a foreign branch of an Indian entity was chargeable to tax in the source jurisdiction, which in this case is UAE. Even though ‘global income’ of an Indian entity is chargeable to tax in India, the treaty provisions avoided double taxation. So, the UAE income was not offered for tax. But, after the 2008 amendment, India got a right to tax,” said Lakhani.

Emphasising this amendment in dismissing the appeal of the assessee company (an engineering firm), the position of the tax office has been unambiguously laid down by the ITAT Mumbai bench comprising Pramod Kumar (vicepresident) and Amarjit Singh (judicial member).

“…we find it difficult to believe that a Big-4 accounting firm, as the assessee’s representative before the DRP (dispute resolution panel), as indeed before us, would really be oblivious of the correct legal position…” said the ITAT ruling. The assessee was advised by persons belonging to a member firm of EY.

In its appeal, the assessee company said that I-T department ought to have excluded Rs 11.91 crore from total income chargeable to tax in the hands of the assessee in India, as this amount represents aggregate of profits earned by assessee’s branches in UAE and Qatar.

However, according to the August 2008 government notification, “…where an agreement entered into by the central government with the government of any country outside India for granting relief of tax, or as the case may be, avoidance of double taxation, provides that any income of a resident of India ‘may be taxed’ in the other country, such income shall be included in his total income chargeable to tax in India in accordance with the provisions of the IT Act, and relief shall be granted in accordance with the method for elimination or avoidance of double taxation provided in such agreement.”

Thus, as per this provision, the profit of Rs 11.91 crore will be fully taxed in India (as the firm paid no tax in UAE). In another treaty country where income tax is levied, the tax paid in India would come down to the extent the assesse pays tax in the foreign country.

Wherever any tax treaty uses the words income “may be taxed”, both the OECD and the UN Model Commentaries on Tax Treaties, as also some eminent authors, such as Prof Klaus Vogel, have clarified that both the source and the resident country have a right to tax that income, said Hitesh D Gajaria, partner, KPMG India.

Source : Times of Iindia